Fannie Mae income calculator integration

The Fannie Mae Income Calculator integration enables rep-and-warranty-backed income calculations for borrowers with self-employed and rental income directly from Ocrolus. It automates the workflow from document ingestion through Encompass export, including extracting rental income data from IRS Schedule E (Form 1040) when applicable, submitting required fields to the Fannie Mae Income Calculator, and returning GSE-backed qualifying income results. This reduces manual entry and rework, improves confidence in income calculations, and supports scalable, compliant underwriting while helping lenders reduce repurchase risk.

Key capabilities

-

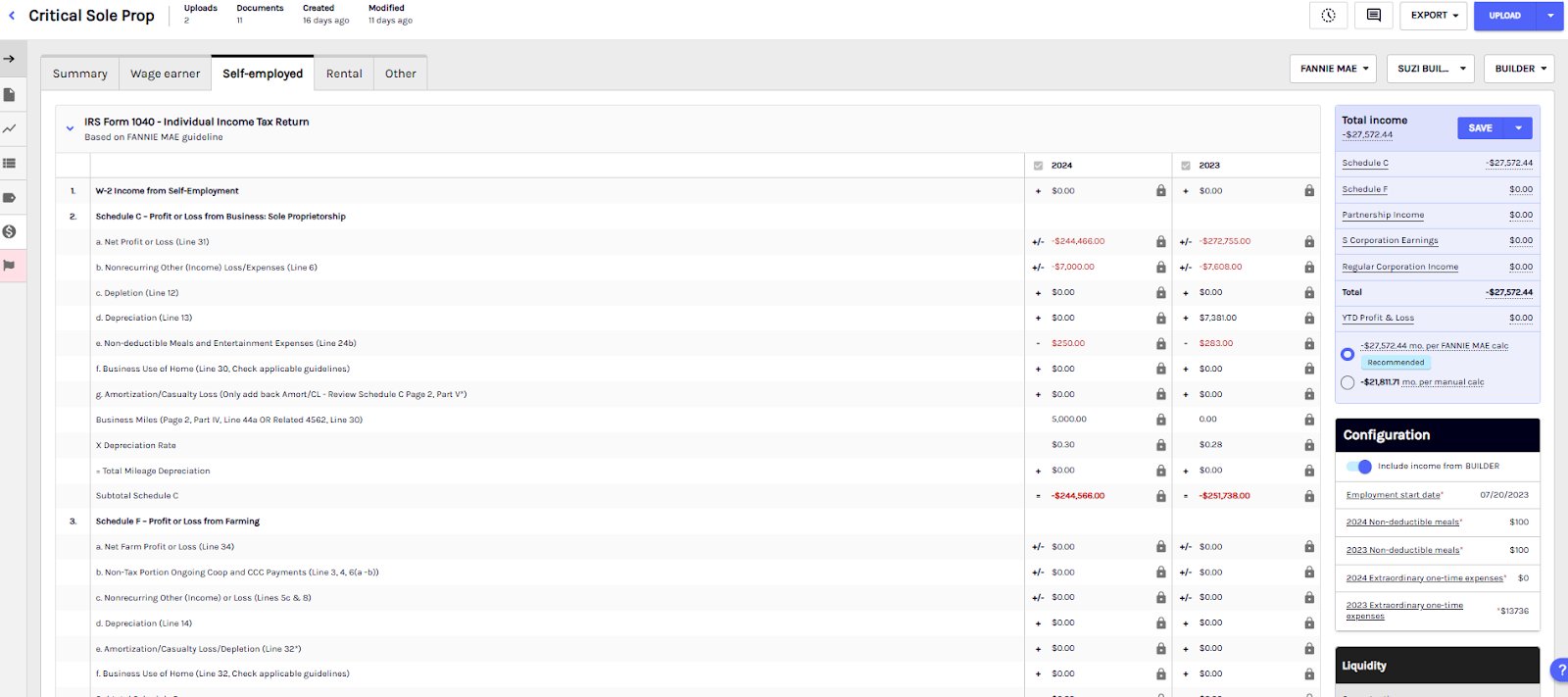

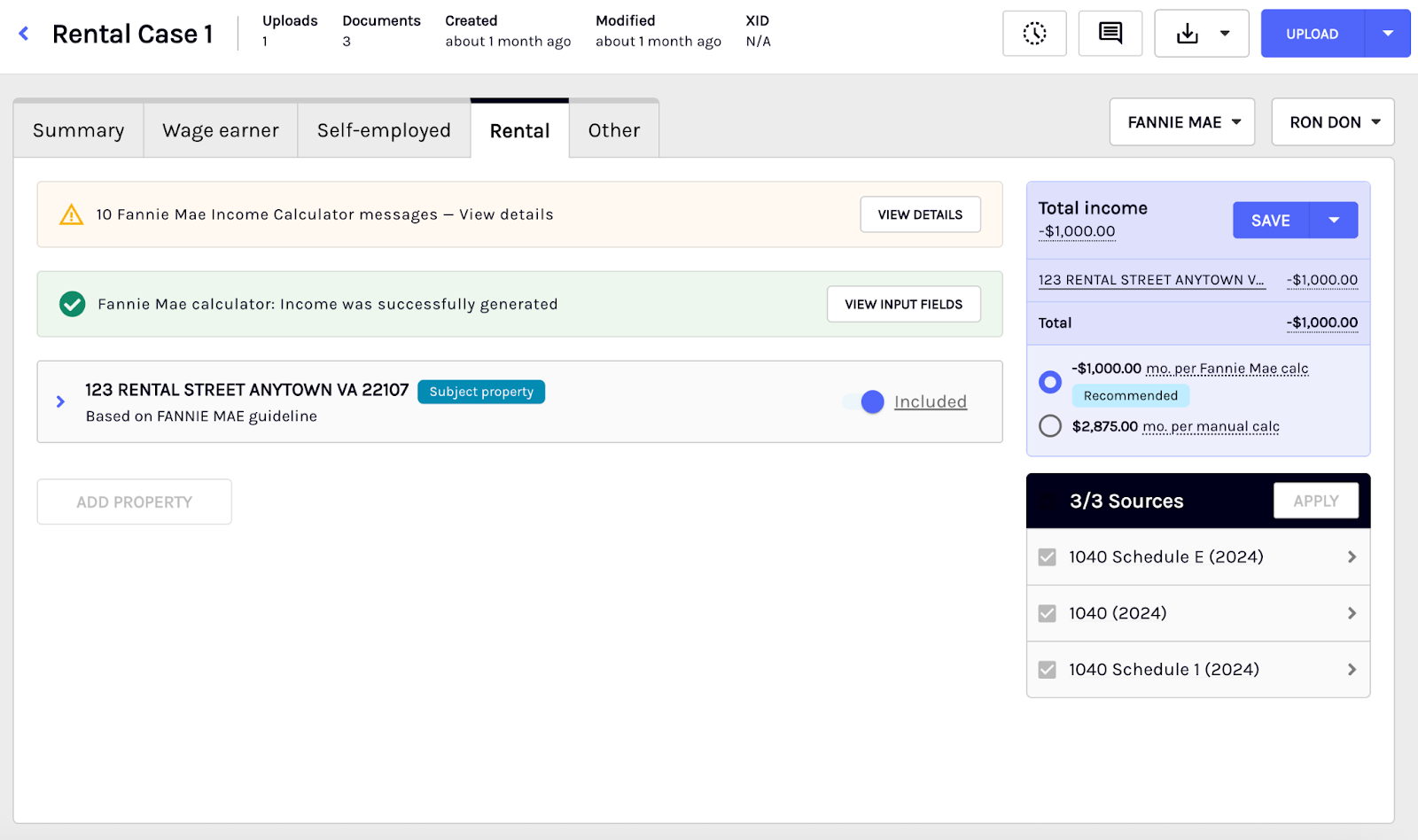

Automated Schedule E extraction: Ocrolus automatically extracts all relevant fields from IRS Form 1040 Schedule E, including rents received, itemized expenses, fair rental days, depreciation, HOA dues, and extraordinary expenses, grouped by property address and tax year for the rental income.

-

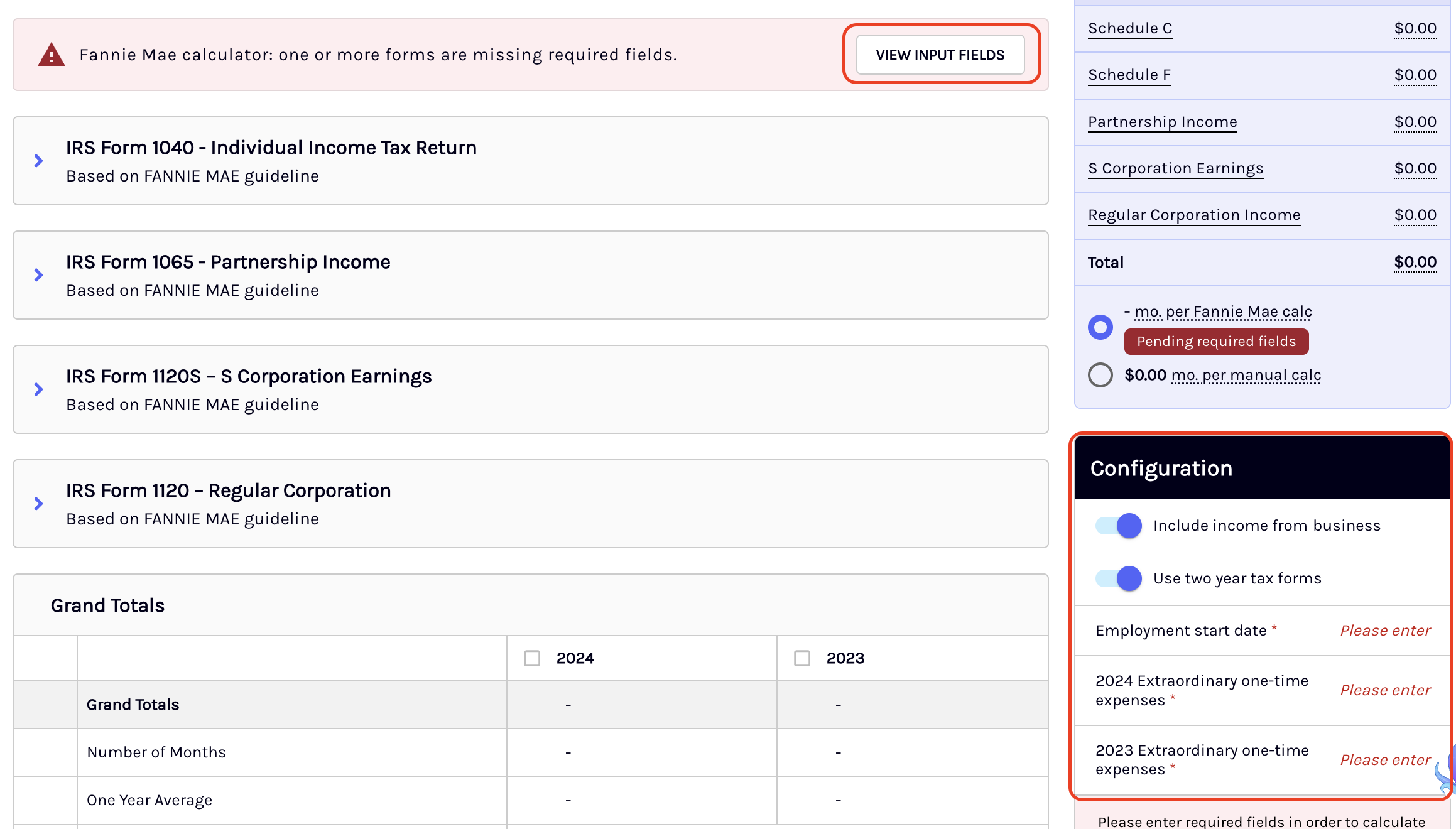

Automated data submission: Once fields are extracted, the system validates completeness of all required inputs and submits the data to the Fannie Mae Calculator. Missing non-documented fields (such as PITIA, property type, or fair rental days detail) are flagged, guiding users to complete them before submission.

-

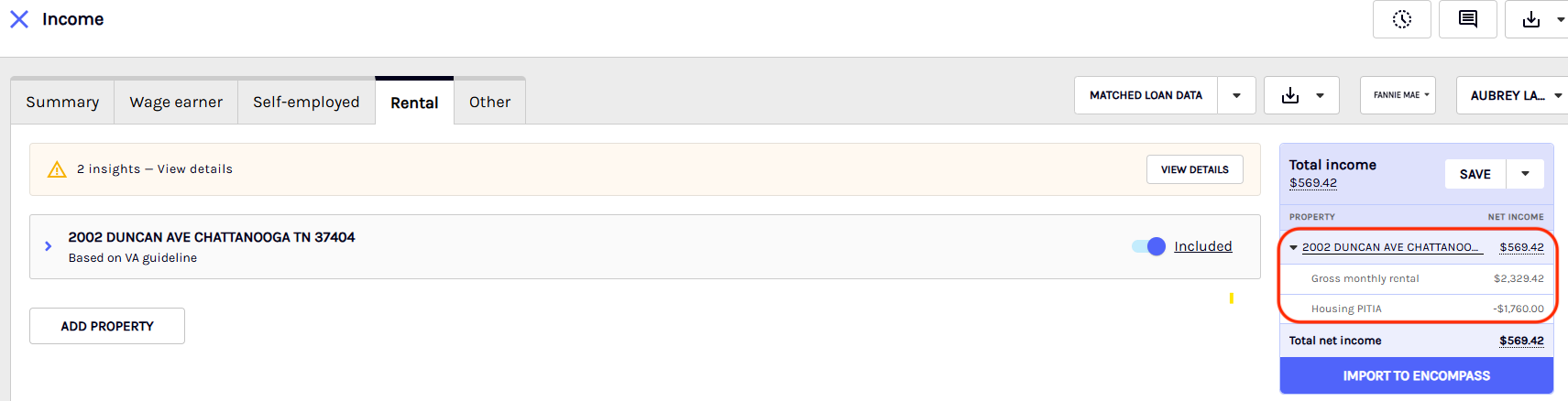

Recommended income display: The Fannie Mae-calculated rental income appears as a dedicated section in Analyze with a Fannie Mae Recommended label, alongside the standard Ocrolus calculation. Inline alerts from Fannie Mae are displayed for transparency and review.

-

Multi-year tax return support: The system supports up to two years of Schedule E data per property. For Fannie Mae guidelines, the most recent tax year is selected by default, with the option to include both years. When both years are selected, the qualifying income is averaged across the selected years.

-

Per-property income breakdown: Each rental property identified on Schedule E is calculated individually, with its own parsed data, calculated results, alerts, and qualifying income. Properties are grouped by address using the Schedule E column qualifier (A, B, C).

-

Property exclusion logic: Properties are automatically excluded from income calculations when they have unsupported property types (codes 7, 8, 9 on Schedule E), missing fair rental days, or exist only in the prior tax year but not the most recent year.

-

Income override warning: When users manually override Fannie Mae-calculated rental income, a warning modal clearly states the rep-and-warranty forfeiture before confirming changes.

-

Re-run income calculations: Users can resubmit rental income to Fannie Mae when supporting documents are updated. The system maintains the same Case File ID, tracks submission history, and supports versioning for compliance.

-

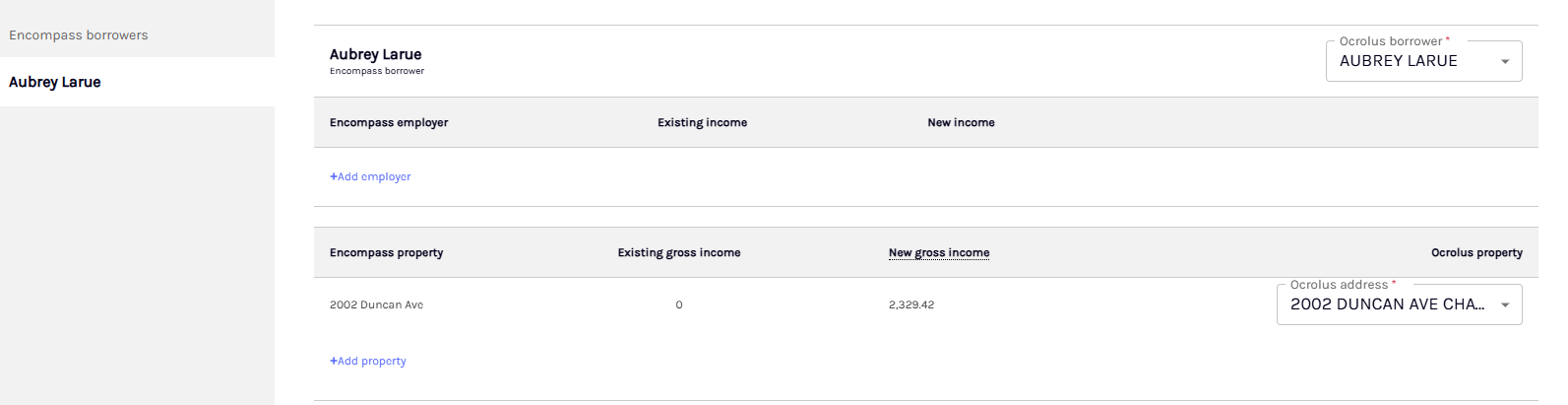

Export to Encompass: Fannie Mae rental income can be exported directly to borrower income fields, and the Case File ID is pushed to the Fannie Mae screen in Encompass for downstream auditability.

Supported income types

The integration supports the following business structures:

Self-employed

Self-employed income is reported under several business structures, including the following:

- Sole Proprietor

- Partnership

- S-Corp

- C-Corp

The Sole Proprietor screen is unique, while other business structures share the same layout except for the right-hand panel, where forms and schedules differ based on the business type.

NoteWe are currently working on displaying the alerts and adding additional requirements for each business structure (as provided by Fannie Mae on July 2025) in line with the new design.

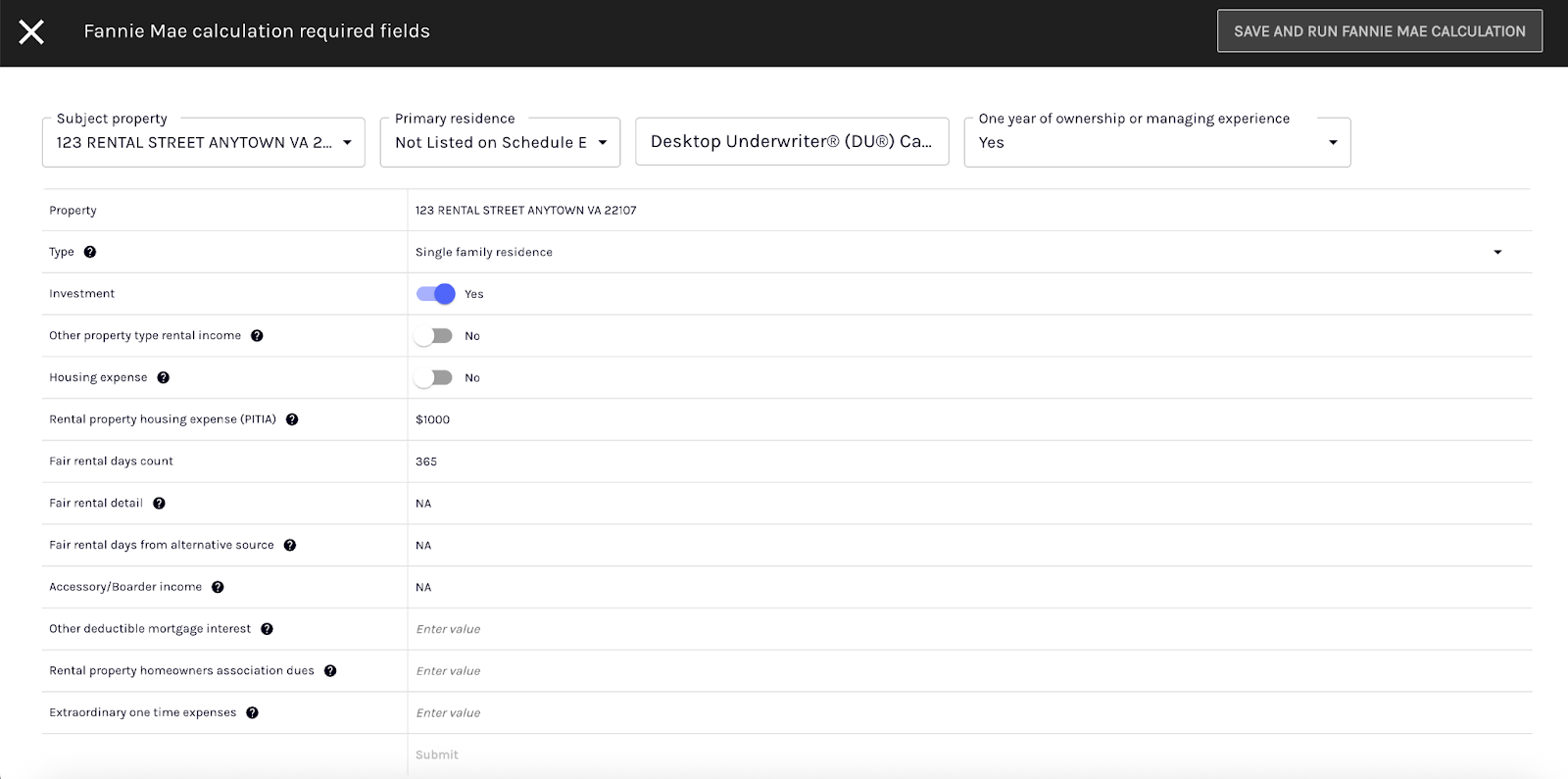

Fannie Mae required fields

The Configuration section includes switches and required inputs that control how income is calculated. Fields marked with an asterisk (*) are required to generate the income result.

| Field | Description |

|---|---|

| Include income from business | A toggle that determines whether business income is included in the total income calculation. Turn it on to include self-employment or business-related income. Turn it off to calculate total income using wage-earner income only. |

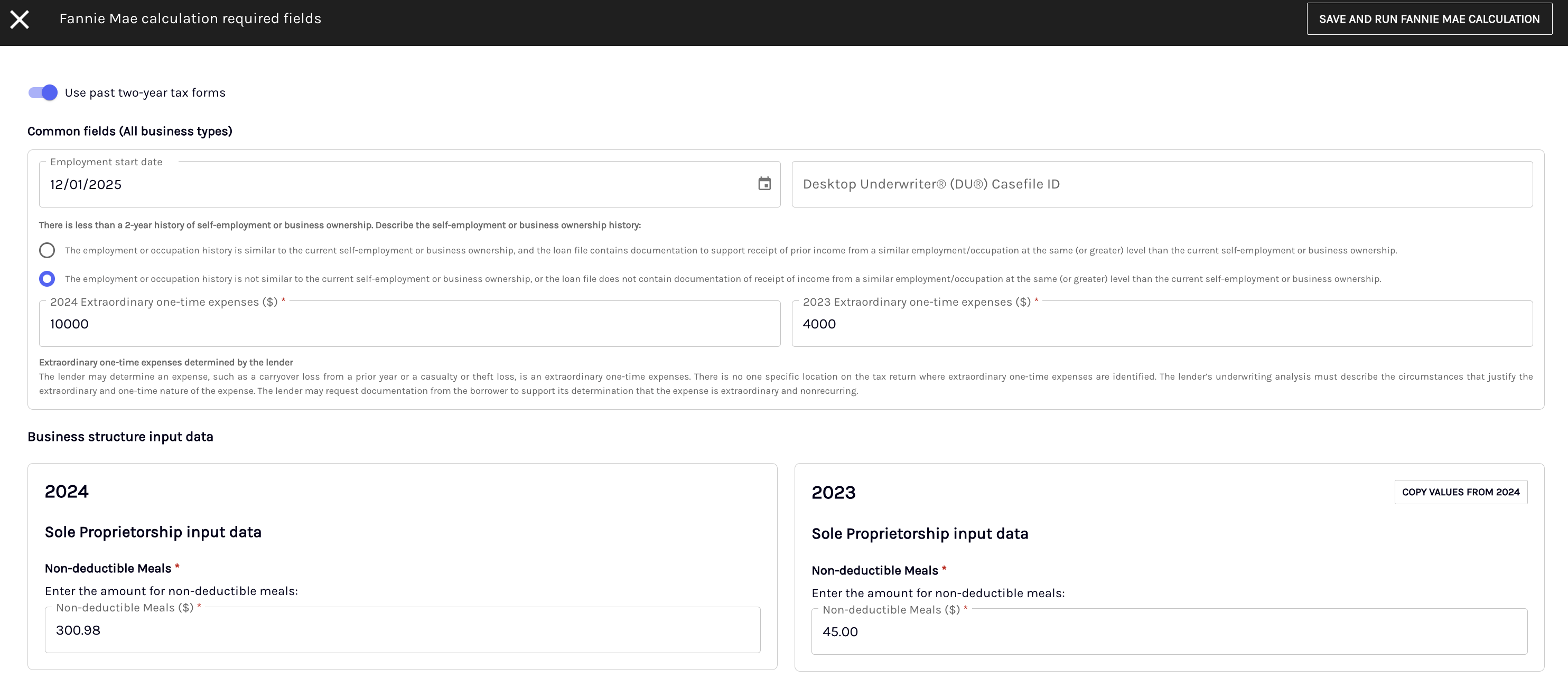

Employment start date * | The borrower’s employment start date. This field helps determine employment history and stability. You must enter this value before total income can be calculated. |

| Use two year tax forms | A toggle that determines whether income is calculated using one year or two years of tax documents. Turn it on to include two years of tax data for a multi-year view of income. Turn it off to calculate income using only the most recent tax year. |

As you complete the required fields, the system can calculate income and display results in Analyze. If any required fields are missing, the screen prompts you to enter them before the calculation can proceed.

Based on your selection, you must enter the required extraordinary one-time expenses for either one year or both years. Extraordinary one-time expenses capture any non-recurring, exceptional expenses in a given tax year that should be considered when calculating income. For example, include one-time business costs, unusual medical expenses, legal settlements, or other exceptional items that may distort the year’s income picture.

TipAlternatively, you can click on the VIEW INPUT FIELDS button to fill in the required field values required for calculation.

As you complete the required fields, the system can accurately calculate total income and reflect any adjustments or exclusions based on your selections. If any required fields are missing, the screen prompts you to enter them before the calculation can proceed.

Rental

The integration supports the following rental property types as configured through the Fannie Mae metadata:

- Single Family Residence

- Multi-Family Residence

- Vacation/Short-Term Rental

- Commercial

- Land

- Royalties

- Self-Rental

- Other

Fannie Mae rental income support is in beta!This section discusses functionality that is in beta. You may occasionally experience unannounced changes or bugs. We'd greatly appreciate your feedback on this feature and its accompanying documentation.

NoteProperties with IRS Schedule E property type codes 7 (Self-Rental), 8 (Royalties), and 9 (Other) on Line 1b are automatically flagged with a Non-Rental Property alert and excluded from rental income calculations. These property types are not eligible for standard rental income treatment under Fannie Mae guidelines.

Forms required for rental income calculation

The following forms are used to extract and validate rental income information for calculation purposes:

Primary form: IRS Form 1040 Schedule E (Supplemental income and loss)

Schedule E is the primary source document for all rental income calculations. The system extracts key rental income and expense fields from Schedule E, grouped by property and tax year.

| Extracted field | Schedule E line reference |

|---|---|

| Property type | Line 1b |

| Fair rental days | Line 2 |

| Rents received | Line 3 |

| Insurance | Line 9 |

| Mortgage interest paid | Line 12 |

| Taxes | Line 16 |

| Depreciation/depletion | Line 18 |

| Other expenses | Line 19 |

| Total expenses | Line 20 |

Supporting forms (Fannie Mae recommended only)

When using the Fannie Mae Recommended calculator, the following additional forms are used to provide broader tax return context:

| Form | Description |

|---|---|

| IRS Form 1040 | U.S. Individual Income Tax Return |

| IRS Form 1040 Schedule 1 | Additional income and adjustments to income |

Appraisal forms (referenced for market rent)

When market rent data is needed for lease- or appraisal-based rental income calculations, the following forms may be referenced:

| Form | Description |

|---|---|

| Form 1007 | Single Family Comparable Rent Schedule |

| Form 1025 | Small Residential Income Property Appraisal |

Fannie Mae required fields

The Configuration section includes switches and required inputs that control how income is calculated. Fields marked with an asterisk (*) are required to generate the income result.

| Field | Description |

|---|---|

Rental property housing payment (PITIA) * | The monthly PITIA payment for the rental property. This value is required for qualifying rental income calculations. |

Fair rental days * | Extracted automatically from Schedule E Line 2 when available. If fair rental days are missing or incomplete, the system prompts the user to provide the required details. |

| Rental property type | A standardized property classification used for rental income calculations and eligibility checks. |

| Extraordinary one-time expenses | Used to capture non-recurring expenses that may impact the income calculation, such as casualty loss or amortization. When present, these may be included in the rental income calculation based on Fannie Mae guidance. |

Gross and net rental income

The Fannie Mae rental income calculator displays two distinct income figures for each property so you can review how qualifying income is derived before exporting to Encompass.

| Field | Label in calculator | Description |

|---|---|---|

| Gross Monthly Rental Income | Equals adjusted monthly rental income | The gross rental income extracted from Schedule E before housing expenses are deducted. |

| Net Monthly Qualifying Income | Monthly qualifying rental income (or loss) | Read-only. Calculated by the system as Gross Monthly Rental Income minus the property Housing PITIA. |

The Net Monthly Qualifying Income field is system-calculated and cannot be edited directly. To adjust the net figure, update the Rental property housing payment (Principal, Interest, Taxes, Insurance, and Association dues) value in the Configuration section.

NoteWhen exporting to Encompass, the gross figure is passed to the Gross Monthly Rental Income field in Encompass. Encompass then applies its own housing expense deduction. Entering a pre netted value in this field would cause housing expenses to be deducted twice, understating qualifying income. The calculator is designed to prevent this.

For Fannie Mae rental properties, the housing expense amount is automatically imported to Encompass via the

maintenanceExpenseAmountfield on export. No manual entry is required.

Rental income calculation approach

Rental income is calculated using a standardized methodology based on Fannie Mae guidelines. The system supports the following two calculation approaches:

| Method | When it’s used | Description |

|---|---|---|

| Step 2A: Schedule E method (Primary) | Default | Uses Schedule E rental income and expenses to calculate adjusted and qualifying rental income. |

| Step 2B: Lease/Appraisal method (Alternative) | Optional | Uses market rent data from appraisal forms or lease agreements instead of tax returns. |

NoteStep 2A (Schedule E method) is the default and primary method. Step 2B is available as an alternative when Schedule E data is not available or when lease/appraisal-based income is required.

Multi-year tax return support

The system supports up to two years of Schedule E data per property. Income treatment varies based on the selected guideline:

| Guideline | Default year selection | Income calculation logic | Alerts |

|---|---|---|---|

| Fannie Mae / Freddie Mac | Most recent year selected | If both years are selected, qualifying income is averaged across the selected years | If only the most recent year is used while two years are available: "One year of the most recent tax returns is currently used for rental income calculation." |

| FHA / VA / USDA | Both years selected | • If only one year is available → that year is used • If income increases year-over-year → average is used • If income decreases year-over-year → most recent (lower) year is used | USDA only: "Rental income was calculated for properties. Verify if borrower has provided rent receipts and signed lease agreement." |

Alerts and validations

The following alerts, categorized by severity, guide underwriters through rental income review:

| Severity | Alert | Trigger condition | Message |

|---|---|---|---|

| HIGH | Missing Fair Rental Days | Fair rental days (Line 2) are missing on Schedule E for a property. | "No rental income computed for property '{address}' as fair rental days are not present on Schedule E." |

| HIGH | Non-Rental Property | The property type on Schedule E (Line 1b) is 7 8 or 9. | "Property '{address}' has unsupported property type '{property_type}'." |

| HIGH | Property Only in Prior Year | The property is reported on the prior year's Schedule E but not on the most recent year's Schedule E. | "Property '{address}' was reported on previous year's tax returns but not reported on recent year's tax returns." |

| HIGH | Missing Yearly Income Data | Only one year of Schedule E data is available when two years are expected under the selected guideline. | "Income was calculated using only 1 year of tax returns for property '{address}'." |

| HIGH | Proof of Receipt Required | Rental income is calculated under USDA guidelines. | "Rental income was calculated for properties. Verify if borrower has provided rent receipts and signed lease agreement." |

| HIGH | Significant Income Change | A significant year over year income change is detected for rental income. | "Significant income change detected for rental income." |

| MEDIUM | Single Year Default | Two years of data are available but only the most recent year is selected by default. | "One year of the most recent tax returns is currently used for rental income calculation." |

| MEDIUM | Line 19 Additional Expenses | Schedule E Line 19 contains expenses that cannot be categorized as HOA dues or extraordinary expenses. | "Schedule E Line 19 contains additional expenses that are not included in the rental income calculation." |

| INFO | Fannie Mae Inline Alerts | Additional alerts are returned when using the Fannie Mae Recommended calculator. | Alerts are displayed inline in Analyze for transparency and review. |

Schedule E Line 19 handling

Schedule E Line 19 ("Other expenses") may include multiple types of rental expenses. When calculating rental income, the system reviews this line and automatically identifies HOA dues and extraordinary one-time expenses such as casualty losses or amortization. These amounts are incorporated into the rental income calculation when applicable. If Line 19 contains additional expenses that cannot be categorized, the system generates a review alert so the underwriter can evaluate whether any further adjustments are needed.

Property exclusion rules

A rental property may be excluded from the income calculation if no Schedule E form is available, if the property type is not eligible under Fannie Mae guidelines (Schedule E Line 1b type codes 7, 8, or 9), if fair rental days are missing for all available tax years, or if the property appears only in the prior tax year but not in the most recent year under Fannie Mae or Freddie Mac guidelines. When a property is excluded, the system generates an alert explaining the reason and sets the qualifying income for that property to zero.

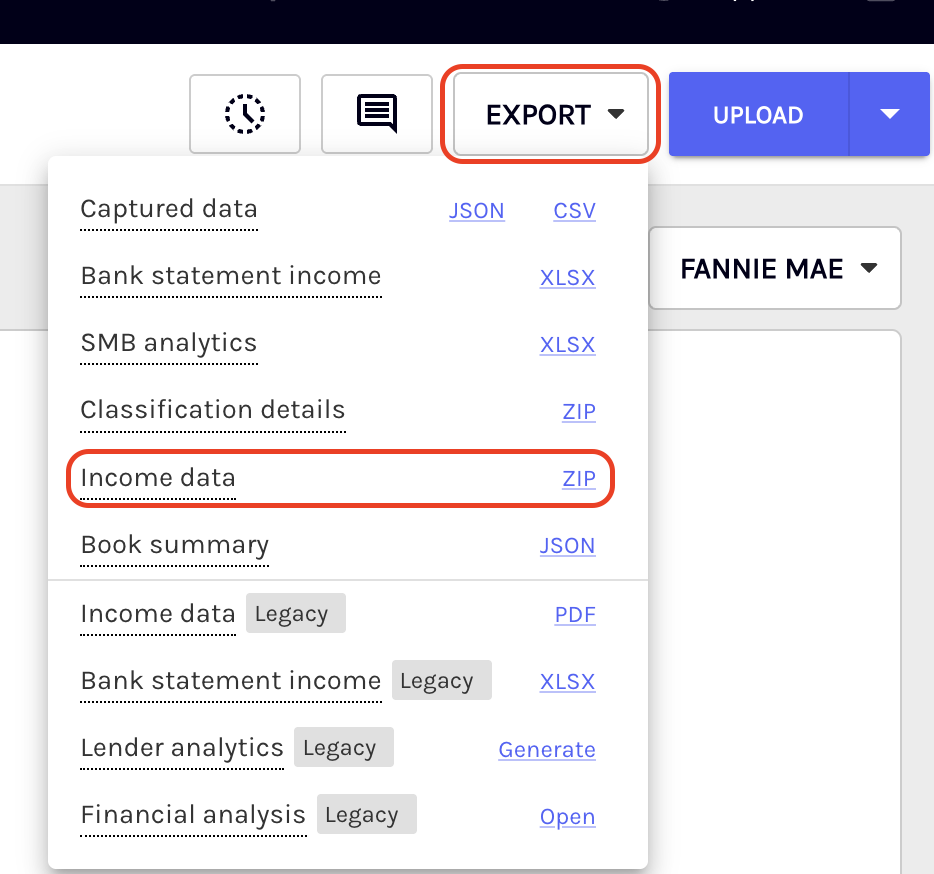

Downloading the Fannie Mae income ZIP

You can download the Fannie Mae income in ZIP format from the same location where the income PDF is usually downloaded. To download the ZIP, click the Export dropdown menu and select the ZIP beside Income data. A ZIP file will be downloaded to your local machine.

Updated 12 days ago