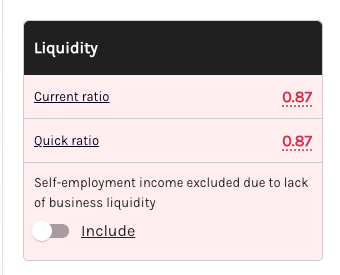

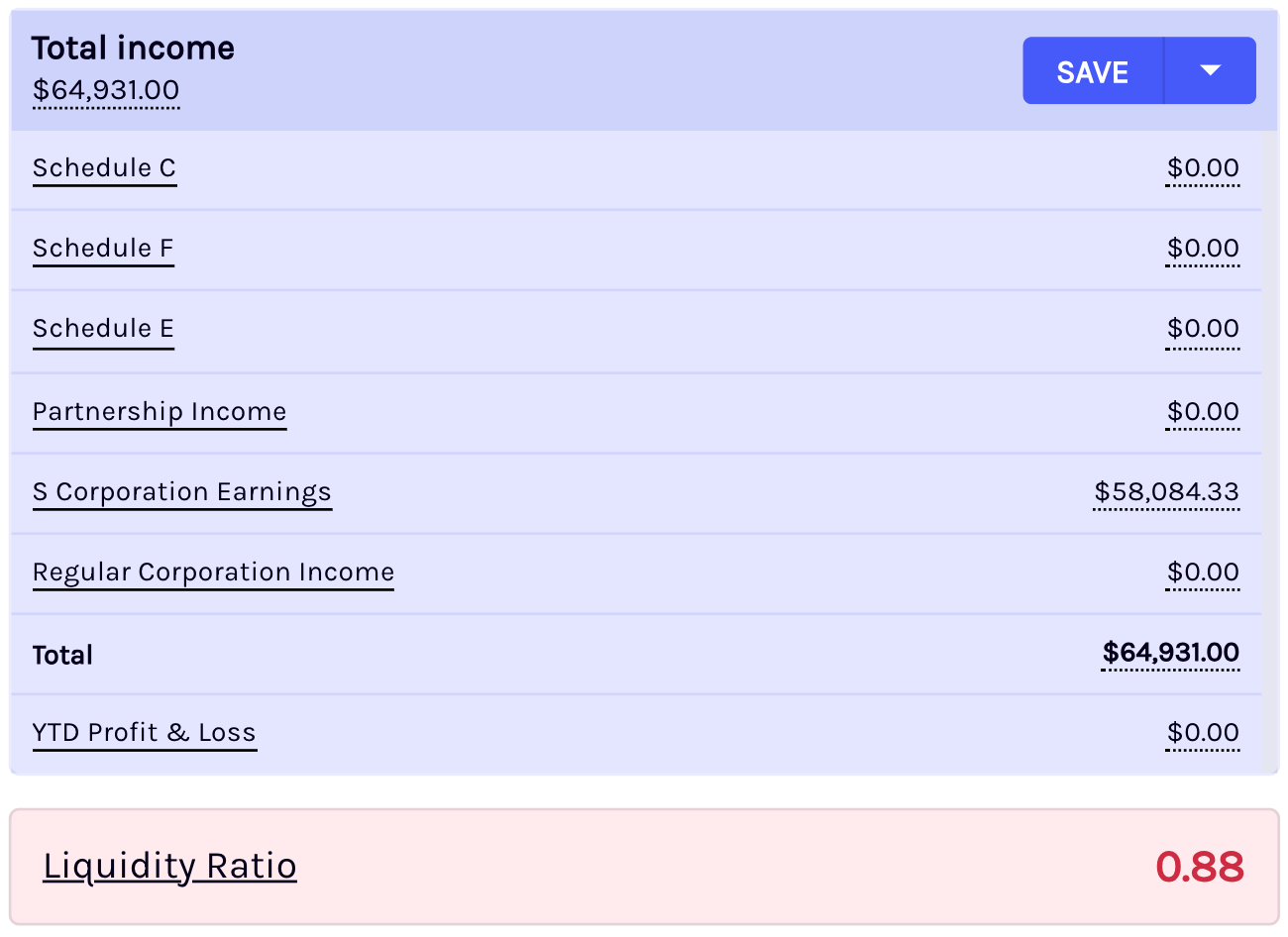

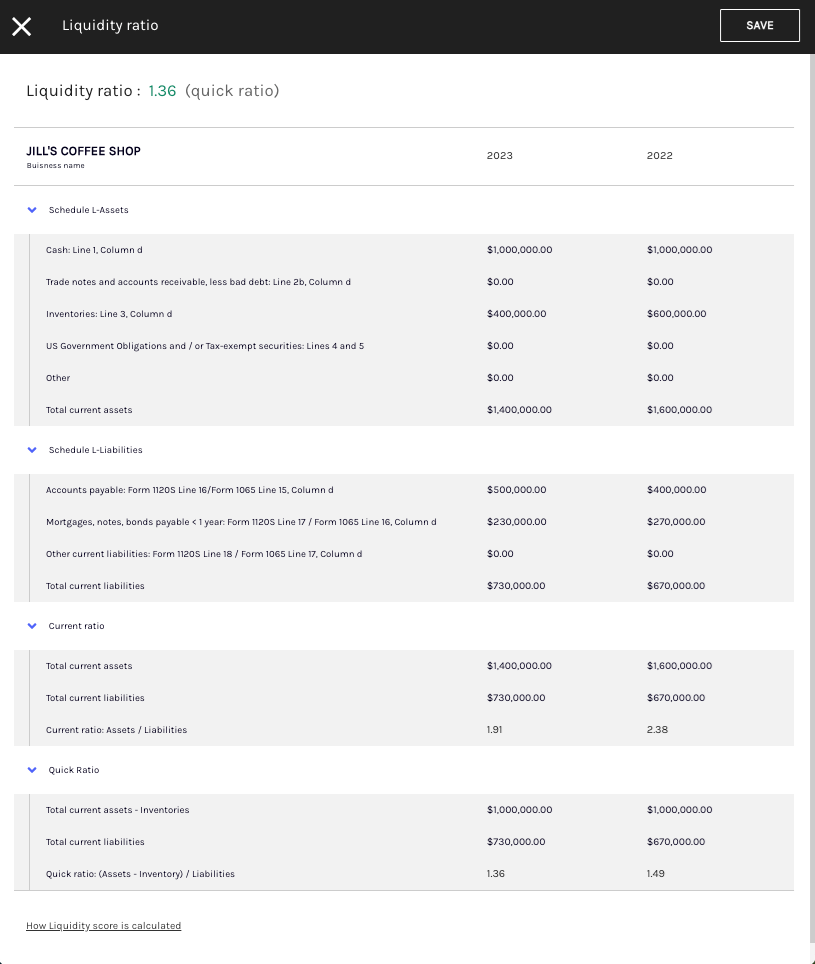

Liquidity ratio

For mortgage lenders, the Liquidity Ratio is computed for self-employed borrowers using 1065, 1120S, or 1120 business tax returns. Three different ratios can be used to calculate a business's liquidity. Ocrolus uses the Quick and Current ratios for the last two years of business returns and presents this on the Income screen to the lender. Ocrolus currently defaults to the Quick Ratio when determining liquidity.

Liquidity-based exclusion for self-employment income

Analyze automatically excludes self-employment income if liquidity ratios suggest potential financial instability:

-

If both the current ratio and quick ratio are below 1, self-employment income is automatically excluded, and an alert is displayed.

-

If the quick ratio is below 1 but the current ratio is above 1, you can manually choose whether to include the income.

Quick ratio

The Quick Ratio (also known as the Acid Test Ratio) excludes inventory from current assets in calculating the proportion of current assets available to meet current liabilities. Below is the formula to calculate the Quick Ratio:

Quick Ratio = (current assets — inventory) ÷ current liabilities

Current ratio

The Current Ratio (also known as the Working Capital Ratio) determines a company's ability to repay short-term obligations by comparing its current assets to its current liabilities. It may be more suitable for businesses that do not rely on existing inventory to generate income. Below is the formula to calculate the Current Ratio:

Current Ratio = current assets ÷ current liabilities

Process insights

For Forms 1065, 1120S, and 1120 related to businesses, Ocrolus reads the corresponding Schedule L, M1, and M2 and calculates the Liquidity ratio from the tax forms for the last two years. The Quick Ratio from the most recent tax return is then displayed on the self-employment income calculation screen for the corresponding business.

Underwriters have the option to inspect the details of the ratio, with a pop-up displaying the specifics of the two-year calculations performed by Ocrolus. Lenders can also choose to manually edit the fields if necessary.

Updated 2 months ago